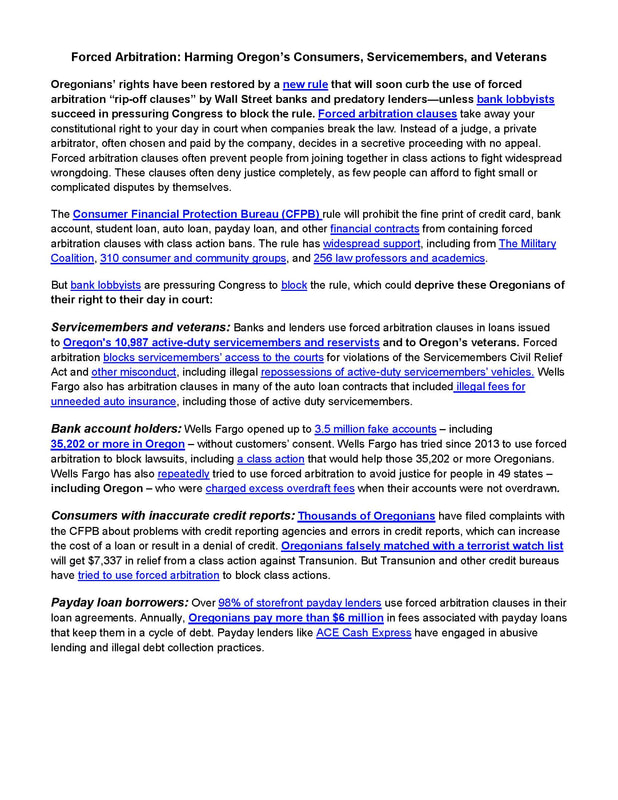

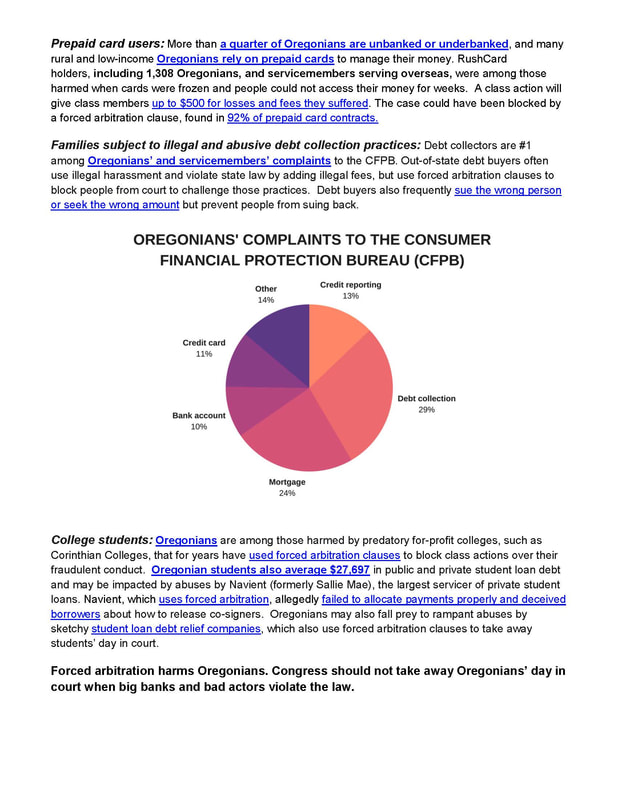

Click on Image to go to NCLC website where you can download as pdf

|

Click on Image to go to NCLC website where you can download as pdf

0 Comments

Things to consider before borrowing a reverse mortgage to delay collecting Social Security By Stacy Canan – AUG 24, 2017 For most people, the amount of money you bring in each month decreases after you retire. Yet your expenses, particularly for health care, may not follow suit. So the question on the minds of many approaching this life stage is: how do I replace or supplement my monthly income when I retire? The most obvious answer might be to claim your Social Security retirement benefits. If you qualify for Social Security retirement benefits, it’s important to think about the best time to claim your benefits. For most people, eligibility for full benefits is between age 66 and 67, depending on the year you were born. Alternatively, you can start to collect benefits as early as age 62, but if you choose to claim early, your monthly benefits may be reduced as much as 30 percent. You can also delay and claim at age 70 to get your maximum monthly benefit. With that in mind, some financial professionals are increasingly promoting that older homeowners consider borrowing a reverse mortgage loan at age 62 in order to delay collecting Social Security. This approach suggests that you use proceeds from the loan to replace the Social Security benefits that you would otherwise receive if you had started collecting Social Security at age 62 until your full benefits age, or later. We looked at different scenarios involving older homeowners for whom their home and Social Security are their main resources and found that generally they are better off if they take their Social Security benefits rather than taking out a reverse mortgage. This is true because, in general, the cost of a reverse mortgage loan will exceed the additional amount of increased Social Security benefits you would collect over your lifetime. That’s because the interest and fees you pay increase each month, and over time those costs wipe out the additional benefit obtained by delaying. When you borrow a reverse mortgage loan, your home is used as a guarantee for the loan, like it is in a traditional mortgage loan. But unlike a traditional mortgage, a reverse mortgage loan is usually repaid when the borrowers no longer live in the home. You won’t make monthly mortgage payments, but you must stay current on paying your real estate taxes and homeowner’s insurance. There are other conditions of the loan that must be met too. If you don’t meet the conditions, the lender can foreclose on your home. If you have the option, working past age 62 is usually a less costly way to delay claiming than borrowing a reverse mortgage loan would be. The additional years of work often provide you more time to save and pay off debts. It may also result in an increase in Social Security benefits by replacing years with low or no earnings, if any, from your earnings record. For those who can’t continue to work, it may be better to accept a lower Social Security benefit amount, rather than owing on a reverse mortgage loan in the future. In addition, the effects of using a reverse mortgage loan to delay collecting Social Security benefits would likely reduce the equity in your home. This loss in equity could limit your options for moving to a new location or handling a large financial shock in the future. We looked at different scenarios involving older homeowners for whom their home and Social Security are their main resources and found that generally they are better off if they take their Social Security benefits rather than taking out a reverse mortgage. New resources We released three new resources to help older homeowners learn what a reverse mortgage is and decide whether borrowing a reverse mortgage is right for them:

If you have a problem with a reverse mortgage, you can submit a complaint online or call us toll free at (855) 411-CFPB (2372), Monday through Friday, 8 a.m. to 8 p.m. ET. We provide complaint-handling services to people in more than 180 languages and to those who are deaf, have hearing loss, or have speech disabilities through the our toll-free telephone number. (This material reposted with permission from the federal Consumer Financial Protection Bureau blog).  For the 7th consecutive year, John Gear Law Office is proud to sponsor the "Empty Bowls" sale at Willamette Art Center, a key yearly fundraiser for Marion-Polk Food Share and our whole community. Always the weekend before Thanksgiving, "Empty Bowls" is where you can find top-class craft art, full of creativity and beauty, by local artists, donated to be sold for very low prices, all to fight hunger. Bring your family and friends and all your holiday shopping lists. As always, Empty Bowls is the weekend before Thanksgiving at Willamette Art Center on the State Fairgrounds in NE Salem (Yellow gate - Silverton Road entrance).   I am proud to have been asked to help write a chapter in the Oregon State Bar's newest practice guide for attorneys, this one aimed at helping attorneys with representing active-duty servicemembers and veterans.

I got to work with a very bright younger attorney and I think that we delivered something that will help Oregon attorneys who have never served more easily find and use the special statutory protections for servicemembers and veterans in federal and Oregon law. Pop Quiz: Q: What's the difference between a fairy tale and a sea story? A: The fairy tale begins "Once upon a time ..." and the sea story begins "When I was on the (ship name) . . . " Great article in The Hill about three big lies the Big Banksters are pushing to persuade Congress to keep consumers from being able to bring class actions against banks who rip off people millions at a time. An excerpt: Big Lie No. 2: Class actions only benefit the attorneys.  We often hear that older Americans want to "age in place." Aging in place means living at home in the community, rather than in an institutional setting, like a nursing facility. This is the choice most people want to make even if they need services and support to do so. When asked to update terms and conditions on the app, I didn't pay attention to what Spotify wanted, though it included the word "arbitration." “Corporate Immunity Bill” Would Let Investment Firms Steal Money from Workers’ Retirement Accounts The Consumer Financial Protection Bureau (CFPB) today announced a new rule to ban companies from using mandatory arbitration clauses to deny groups of people their day in court. Many consumer financial products like credit cards and bank accounts have arbitration clauses in their contracts that prevent consumers from joining together to sue their bank or financial company for wrongdoing. By forcing consumers to give up or go it alone – usually over small amounts – companies can sidestep the court system, avoid big refunds, and continue harmful practices. The CFPB's new rule will deter wrongdoing by restoring consumers' right to join together to pursue justice and relief through group lawsuits.

AT&T: it's not "forced arbitration" because no one forced you to have broadband Student Loan Collections Push Older Borrowers into Poverty Des Moines Register EDITORIAL: Trump protects nursing homes at seniors' expense Last week, the Centers for Medicare and Medicaid Services proposed a rule rescinding an Obama-era regulation prohibiting nursing homes from requiring patients and their families to sign binding arbitration agreements. Signing those agreements, which are frequently part of admission paperwork, means giving up the right to sue a facility. Criminal Bank Seeks to Use Forced Arbitration to Avoid Justice

MEDIA ADVISORY After Promising to Make Things Right, Wells Fargo Asks Judge to Kick Defrauded Consumers out of Court June 6, 2017 Contact: Amanda Werner, awerner@ourfinancialsecurity.org, (202) 973-8004 Tomorrow, a federal judge in Utah will decide whether more than 50 consumers defrauded by banking giant Wells Fargo in its fake account scandal will be forced to pursue claims one-by-one in a secret arbitration system. As the bank loudly promises to restore consumer trust, Wells Fargo is quietly insisting that defrauded customers should be barred from holding it accountable in court by pointing to “ripoff clauses” buried deep in its contracts. Customers represented in Mitchell v. Wells Fargo argue that the bank cannot use its contracts as a shield against liability for systemic fraud. While forced arbitration has been upheld in many contexts, the customers claim they could not reasonably understand that signing a standard agreement for one product would block them from suing over a separate account they never agreed to open. Indeed, at least one consumer represented in this class action never even banked with Wells Fargo or signed an account contract. Experts from the Fair Arbitration Now (FAN) coalition are available to comment on this hearing, as well as a forthcoming rule from the Consumer Financial Protection Bureau (CFPB) that would restrict the use of arbitration clauses in future consumer financial contracts. Please contact awerner@ourfinancialsecurity.org to speak with an expert in the FAN coalition. ### Sponsored in part by John Gear Law Office Come hear the story about what happens when politicians in one of the most advanced nations in the world decide that the answer to social unrest and economic woes are nationalism and militarism rather than justice and the rule of law. Every single seat should be filled for this talk. If you have a teen or young adult close to you, bring them with you so they can hear -- as will only be possible for a few more years -- from a survivor of what happens when a mighty nation is more concerned with being feared for its power than respected for its wisdom.  This is well worth a 20 minute look and then taking action by commenting in support of STRONG, ENFORCEABLE NET NEUTRALITY BASED ON TITLE II of the FCC Act of 1934  Great resource for unbiased financial literacy and consumer protection education: The FoolProof Foundation.

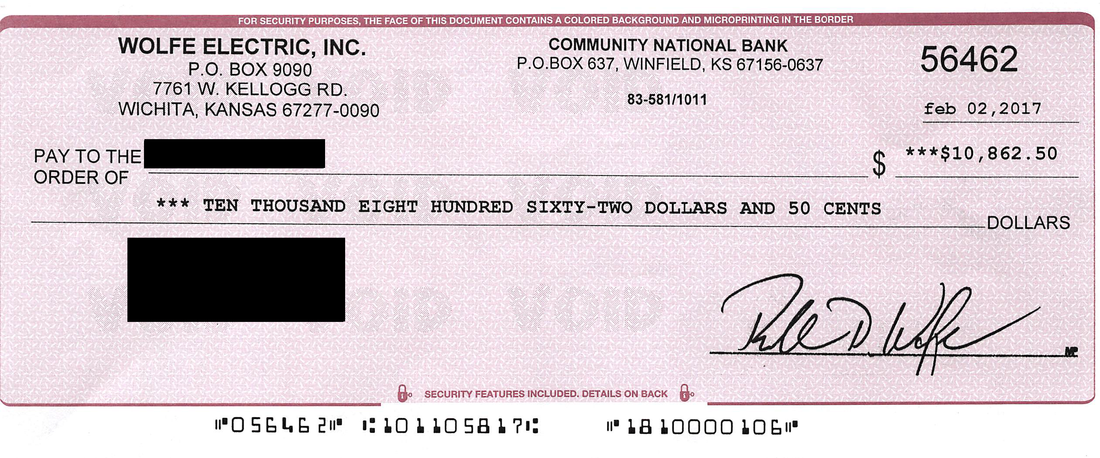

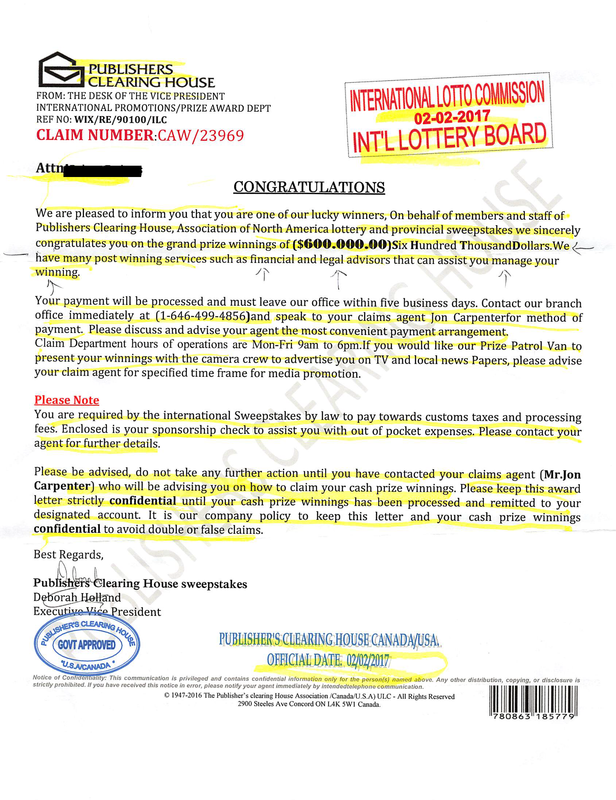

Wells Fargo: Wanting to Appear Contrite, While Just Doing More Fraud The insistence by Wells Fargo that the victims of its bogus account-opening scandal seek redress via arbitration, rather than in court, remains the best indication that the bank’s promise to “make things right” for those customers is fake. Northwest Hub is putting together 40 complete reclaimed bicycles and kit sets (lights, locks, helmets, etc.) for use by some of Salem's new residents, resettled refugees. $100 gives a new neighbor a way to get to school and work and on the path to independence and success. Join John Gear Law Office in supporting this great community nonprofit venture. Call the Oregon Attorney General's Consumer Protection Complaint Hotline at 877-877-9392 and report the business! The Consumer Review Fairness Act protects consumers’ ability to share their honest opinions about a business’s products, services, or conduct in any forum – and that includes social media. The terrific organization "Consumers for Auto Reliability and Safety" (aka CARS) has put an awful lot of work into figuring out how to make the purchase of a used car as successful for the buyer as possible -- here is their best wisdom, in one easy list. Having published a number of these over the years, let me repeat one point: If you think you can't afford an independent pre-purchase inspection for any car you are seriously interested in, you can't afford the car, period. Letting the dealer suggest or pick the mechanic to inspect the car you are thinking about buying for you or, even worse, relying on the dealer's own opinion or that of the dealer's mechanic is like letting your blackjack opponent decide whether you should take additional cards: you will end up busted every time. Car dealers are NOT in the business of helping you buy the best car at the lowest price. Their only business is making as much money as they can, and used cars are just the means to that end. In other words, used car dealers are in the business of selling you the least car they can unload on you at the highest price possible, with as much unnecessary garbage packed into the contract as you will swallow. Making as much money from each customer as possible is the only religion of the used car dealer, and if some car salesman or finance manager has you thinking otherwise -- well, pardner, remember the old saying: if you don't know who the sucker at the poker table is, it's you. The only people who get the better cars for the best prices are the people who follow the 11* steps below. How to Buy a Used Car Clients called me today about a "You Have Won" letter they got -- or thought they got today. They struggle with age-related issues, but the check in the envelope was so well-done that it could likely fool 99 out of 100 people into thinking it was genuine. Thankfully, the letter that came with the check gave off such a strong stench of scam that the clients were able to resist taking the bait long enough to call me instead of calling the phone number in the letter (or, worse, depositing the check and spending from it). This is a really high-quality fraudulent check scam, a tribute to the wonders of digital printing. Glad the scammers' cover letter was so terrible. But it’s a warning — with a check this good, eventually they will come up with an equally good cover letter. Remember always, always, always: Money NEVER calls you on the phone or Arrives in your Mailbox Out of the Blue   |

AuthorJohn Gear Law Office - Categories

All

Archives

December 2022

|

|

Lawyerly Fine Print:

John Gear Law Office LLC and Salem Consumer Law. John Gear Law Office is in Suite 208B of the Security Building in downtown Salem at 161 High St. SE. That is right across High Street from the Elsinore Theater, a half-block south of Marion County Courthouse.

John Gear is only licensed to practice law in Oregon. This site may be considered advertising under Oregon State Bar rules. There is no legal advice on this site so do not take anything you read here as advice for your particular problem or situation. And I do not represent you and I am not your attorney unless you have hired me with a representation agreement. While I do want you to consider me when you seek an attorney, you should not hire any attorney based on brochures, websites, advertising, or other promotional materials. All original content on this site is Copyright John Gear, 2010-2022. |

RSS Feed

RSS Feed