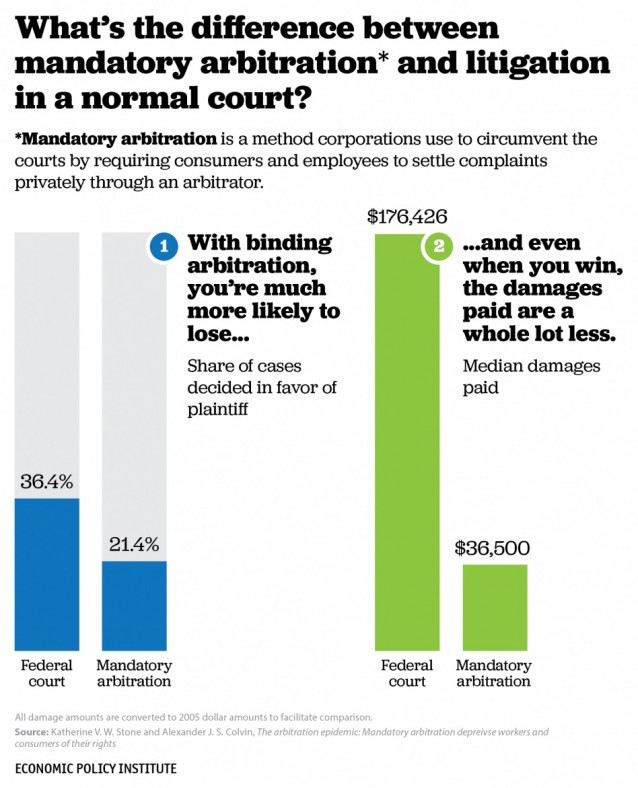

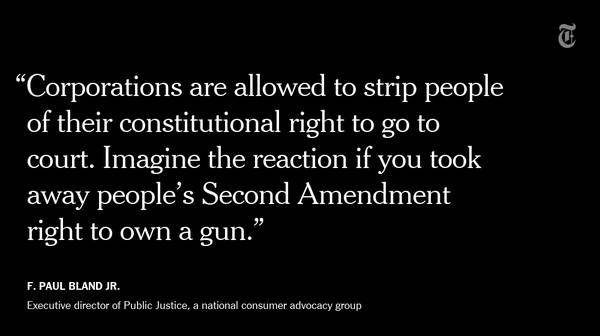

Paul Bland, executive director of Public Justice, flags a new article by two NY Times reporters who have latched onto the story of the century: how corporations are using arbitration clauses to make crime pay.

Jessica Silver-Greenberg and Michael Corkery have done it again, with a horrific example of how nursing homes can neglect patients and then cover up their misdeeds with forced arbitration. Absolutely intense illustration of the intensity of the damage these fine print contracts cause. If millions of people read this story, it will be enormously helpful.

http://nyti.ms/20NhGeE

RSS Feed

RSS Feed